What Is an Investment and How It Can Help Build Wealth

|

Getting your Trinity Audio player ready...

|

If you’ve ever wondered what is an investment and how it can help build wealth, you’re not alone. Most people grow up learning how to earn money and how to spend it, but almost nobody teaches us how to make money work for us. Understanding how it can help build wealth isn’t about complicated math or having a finance degree — it’s about understanding a few core principles and applying them consistently over time.

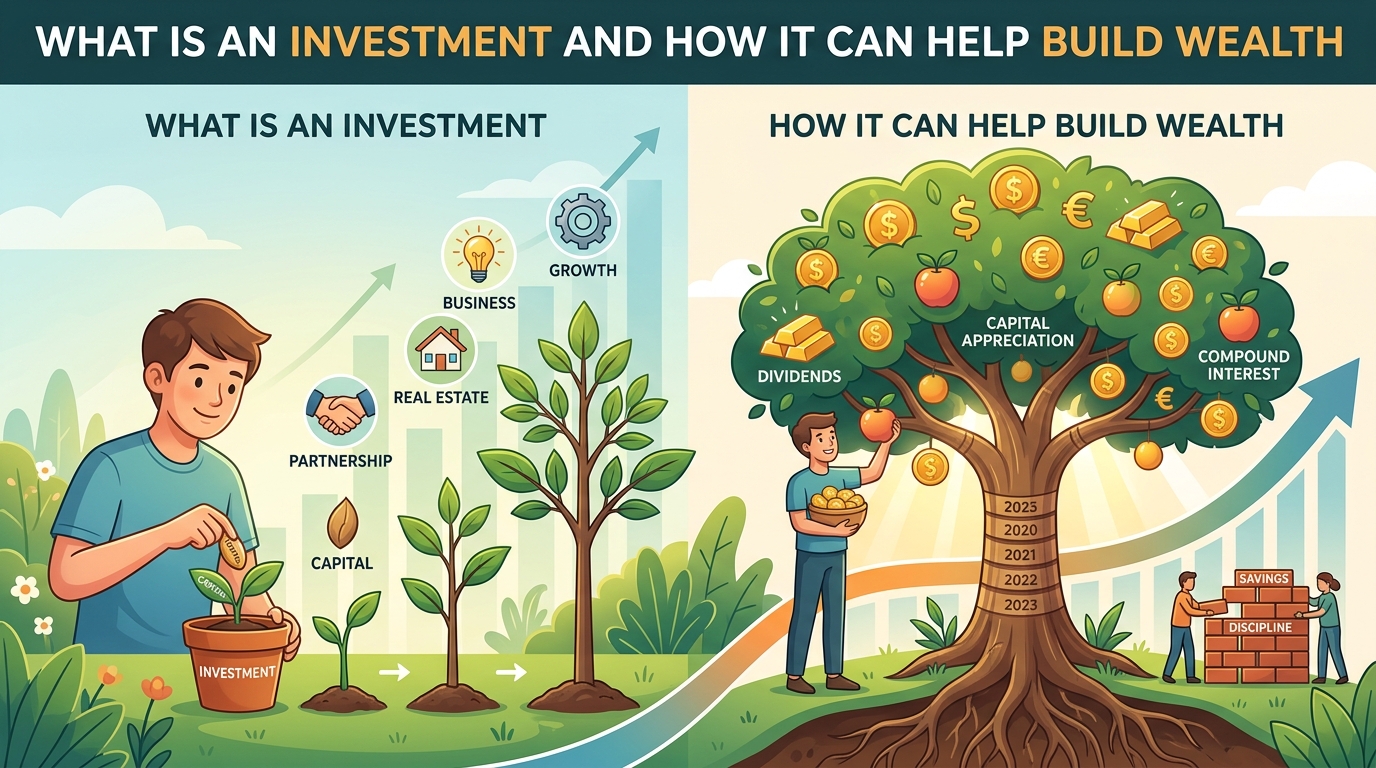

At its simplest, an investment is the act of putting money into something today with the expectation that it will grow in value or generate income over time. This could be stocks, real estate, bonds, a small business, or even your own education. The key difference between saving and investing is that saving protects your money, while investing puts it to work.

And that’s precisely how it can help build wealth — by allowing your money to multiply rather than just sit still.

The Real Difference Between Saving and Investing

Many people confuse saving with investing, and this confusion can cost decades of potential growth. Saving means putting money aside in a safe place, like a checking or savings account, where it’s protected but barely grows. Investing means accepting some level of risk in exchange for the potential of higher returns.

Neither is wrong — they serve different purposes.

Think of saving as your financial safety net and investing as your financial engine. You need both. A common mistake is keeping large amounts of money in a savings account for years, thinking it’s “safe,” while inflation quietly erodes its purchasing power.

This is one of the silent ways people lose wealth without even realizing it.

- Savings: low risk, low return, high liquidity

- Investments: variable risk, potential for higher returns, often less liquid

- Inflation: the hidden cost of not investing

How Compound Growth Works in Your Favor

One of the most powerful concepts in finance is compound growth — sometimes called the “snowball effect.” When your investment earns a return, that return gets added to your original amount. The next time it grows, it grows based on the new, larger total.

Over years or decades, this creates exponential rather than linear growth.

Here’s a practical example: if you invest $200 a month starting at age 25 with an average annual return of 7%, by age 60 you could have well over $300,000 — and more than half of that would come purely from growth, not from money you actually deposited. This is exactly how it can help build wealth even for people who don’t start with large amounts of capital.

The lesson here is simple but often ignored: time matters more than the amount. Starting small but starting early almost always beats waiting until you have “enough” to invest a large sum.

Common Types of Investments Explained Simply

When people first explore investing, the number of options can feel overwhelming. But most investments fall into a few broad categories, each with its own risk and reward profile. Understanding these basics is essential before diving into any specific strategy.

- Stocks: Ownership shares in a company, with potential for growth and dividends, but higher volatility.

- Bonds: Loans to governments or companies that pay fixed interest, generally more stable than stocks.

- Real Estate: Physical property that can generate rental income and appreciate over time.

- Mutual Funds and ETFs: Baskets of investments that offer diversification without needing to pick individual assets.

- Retirement Accounts: Tax-advantaged accounts designed specifically for long-term wealth building.

Each of these tools can play a role in how it can help build wealth, depending on your goals, timeline, and comfort with risk. There’s no single “best” investment — the best one is the one that fits your personal situation and that you’ll actually stick with through market ups and downs.

Why Diversification Is Not Just a Buzzword

You’ve probably heard the phrase “don’t put all your eggs in one basket,” and in investing, this isn’t just a cliché — it’s a survival strategy. Diversification means spreading your money across different types of assets, industries, and even geographic regions so that a downturn in one area doesn’t wipe out your entire portfolio.

Imagine someone who invested their entire savings into a single company’s stock because it was performing well. If that company faces unexpected trouble, their whole financial future could be at risk. Now imagine that same amount spread across dozens of companies through an index fund — a single company’s struggles barely make a dent.

This is one of the most practical lessons in personal finance: diversification doesn’t guarantee profits, but it significantly reduces the chance of catastrophic loss. It’s a foundational piece of how it can help build wealth in a sustainable, less stressful way.

Setting Realistic Financial Goals Before You Invest

Before putting a single dollar into any investment, it’s worth asking: what am I actually investing for? Retirement, a house down payment, your children’s education, or simply financial independence? Your goals shape your entire strategy, including how much risk you can afford to take and how long you can leave your money invested.

Short-term goals (less than 3 years) generally call for safer, more liquid investments, since you can’t afford major losses right before you need the money. Long-term goals (10+ years) can typically handle more volatility because there’s time to recover from market dips.

Writing down your goals — even informally — turns investing from an abstract concept into a concrete plan. It also helps you avoid emotional decisions, like panic-selling during a market downturn simply because you forgot why you started investing in the first place.

The Role of Risk Tolerance in Building a Portfolio

Risk tolerance is deeply personal, and there’s no shame in being conservative or aggressive — what matters is honesty with yourself. Some people can watch their portfolio drop 20% and feel calm, knowing it’s temporary. Others lose sleep over a 5% dip.

Neither reaction is “wrong,” but it should inform your investment choices.

A portfolio that doesn’t match your true risk tolerance is a recipe for bad decisions. If you’re too aggressive for your comfort level, you might sell in a panic during a downturn, locking in losses. If you’re too conservative, you might miss out on growth needed to reach your goals — undermining how it can help build wealth over the long run.

A good rule of thumb: if a market drop would make you check your portfolio every hour and lose sleep, your allocation is probably too aggressive for your personality, regardless of what any calculator says is “optimal.”

Practical Steps to Start Investing Today

Knowledge without action doesn’t build wealth. If you’re ready to move from learning to doing, here are some practical, beginner-friendly steps that apply regardless of where you live or how much money you’re starting with.

- Build a small emergency fund first — ideally 3 to 6 months of essential expenses.

- Pay off high-interest debt before investing aggressively, since guaranteed “returns” from debt payoff often beat market returns.

- Open an investment account with a reputable broker or platform.

- Start with low-cost, diversified index funds if you’re unsure where to begin.

- Automate contributions so investing becomes a habit, not a decision you make every month.

- Review your portfolio periodically — but avoid checking it daily, as this can lead to emotional decisions.

One personal observation worth sharing: the people who tend to build the most wealth over time aren’t necessarily the smartest investors — they’re the most consistent ones. Automating contributions removes willpower from the equation entirely, which is often the deciding factor between success and abandonment.

Mistakes That Quietly Undermine Long-Term Wealth

Even well-intentioned investors fall into traps that slow down their progress. Recognizing these patterns early can save years of lost growth and unnecessary stress.

- Trying to time the market: Studies consistently show that staying invested beats trying to predict highs and lows.

- Ignoring fees: High management fees can quietly eat into returns over decades.

- Chasing trends: Jumping into whatever is popular often means buying high and selling low.

- Neglecting taxes: Using tax-advantaged accounts when available can significantly boost net returns.

- Lack of patience: Wealth building is a marathon, not a sprint, and impatience often leads to costly mistakes.

Avoiding these pitfalls doesn’t require expert-level skill — just awareness and discipline. In many ways, how it can help build wealth depends less on finding the “perfect” investment and more on avoiding unforced errors over time.

The Emotional Side of Investing Nobody Talks About

Personal finance is often presented as purely mathematical, but emotions play a massive role in investment success. Fear during downturns and greed during booms have derailed more portfolios than bad strategy ever has. Learning to manage your emotional reactions is just as important as understanding asset allocation.

One helpful mindset shift is viewing market downturns not as disasters, but as opportunities. If you’re investing for decades, lower prices simply mean you’re buying assets at a discount. This reframe takes practice, but over time it can transform how you experience market volatility entirely.

Building this kind of emotional resilience is, in its own quiet way, part of how it can help build wealth — because the strategy only works if you’re psychologically able to stick with it through difficult periods.

Long-Term Mindset: The True Foundation of Wealth

Perhaps the single most underrated factor in successful investing is mindset. People who view investing as a get-rich-quick scheme are often disappointed and discouraged within months. People who view it as a decades-long journey tend to stay the course — and end up far ahead.

This long-term perspective changes how you react to news, market crashes, and even your own mistakes. A bad month becomes irrelevant when viewed against a 30-year horizon. This shift in perspective is, at its core, the engine behind how it can help build wealth for ordinary people without extraordinary incomes.

If you’re looking for additional reading on foundational personal finance concepts, resources like Investor.

gov offer free, unbiased educational material that can complement what you’ve learned here.

Final Thoughts Before You Take Action

Investing isn’t reserved for the wealthy, the highly educated, or people with finance backgrounds. It’s a skill — and like any skill, it improves with practice, patience, and consistency. The earlier you start, the more time works in your favor, and the less pressure you’ll feel to take big risks later in life.

What matters most isn’t finding a “secret” strategy, but understanding the fundamentals well enough to stay calm, stay consistent, and stay invested through both good times and bad. That, ultimately, is how it can help build wealth — not through luck, but through informed, steady action over time.

Now it’s your turn: have you started investing yet, or are you still on the fence? What’s holding you back — lack of knowledge, fear of risk, or simply not knowing where to start? Share your thoughts and questions in the comments below — your experience might help someone else take their first step.

Frequently Asked Questions About Investing and Wealth Building

What is the minimum amount needed to start investing?

Many platforms allow you to start with very small amounts, sometimes as little as $1 to $50, especially through fractional shares or low-cost index funds.

Is investing risky?

All investments carry some level of risk, but diversification, time, and a long-term mindset can significantly reduce that risk over the years.

How long should I keep my money invested?

Generally, the longer your time horizon, the better your chances of riding out market volatility and benefiting from compound growth.

Can investing really help build wealth for average earners?

Yes — consistency, even with modest contributions, has historically allowed average earners to build significant wealth over decades.

Should I pay off debt before investing?

High-interest debt should usually be addressed first, since the guaranteed “return” from eliminating it often exceeds typical investment returns.

Michael Rowan is a dedicated writer and researcher specializing in Personal Finance and Investments. With a passion for helping individuals make smarter financial decisions, he creates informative and practical content designed to simplify complex financial topics.