The Importance of Diversification in Investments and How to Apply It

|

Getting your Trinity Audio player ready...

|

If you’ve spent any time reading about investing, you’ve probably heard the phrase “don’t put all your eggs in one basket” more times than you can count. It’s a cliché for a reason: it works. But understanding diversification in theory and actually knowing Investments and How to Apply It in your own portfolio are two very different things, and that gap is where most beginners get stuck.

This article goes beyond the surface-level advice. We’ll explore why diversification matters so much, what happens when it’s done poorly, and most importantly, walk through practical steps for Investments and How to Apply It in a way that actually fits your goals, timeline, and risk tolerance. By the end, you’ll have a clear framework for thinking about diversification that goes well beyond “just buy a bit of everything.

“

What Diversification Really Means Beyond the Basics

At its core, diversification is the practice of spreading your investments across different assets so that no single investment has the power to significantly damage your overall portfolio. But here’s where many people misunderstand the concept: owning ten different stocks isn’t necessarily diversified if all ten companies are in the same industry, same country, and react to the same economic events in similar ways.

True diversification considers correlation, meaning how different investments move in relation to each other. Two assets that tend to move in opposite directions, or at least independently, provide more protection than two assets that tend to rise and fall together. This is the deeper layer of Investments and How to Apply It that separates a genuinely diversified portfolio from one that just looks diversified on the surface.

Why Concentration Risk Is More Dangerous Than It Seems

Concentration risk happens when too much of your portfolio depends on the performance of a single asset, sector, or market. It’s easy to fall into this trap without realizing it, especially when you work for a company and also hold significant stock in that same company through employee stock plans or 401(k) contributions.

History offers plenty of cautionary tales. Employees who held large amounts of company stock in firms that later collapsed often lost both their jobs and a significant portion of their retirement savings simultaneously, a devastating double hit. This is precisely the kind of scenario that diversification is designed to prevent, by ensuring that no single point of failure can derail your entire financial future.

Even outside of employer stock, concentration risk can creep in through enthusiasm. Maybe you love a particular tech company’s products, so you keep buying more of its stock. Before long, that single company represents 30% or 40% of your portfolio without you consciously deciding it should.

Investments and How to Apply It properly means periodically checking for these blind spots.

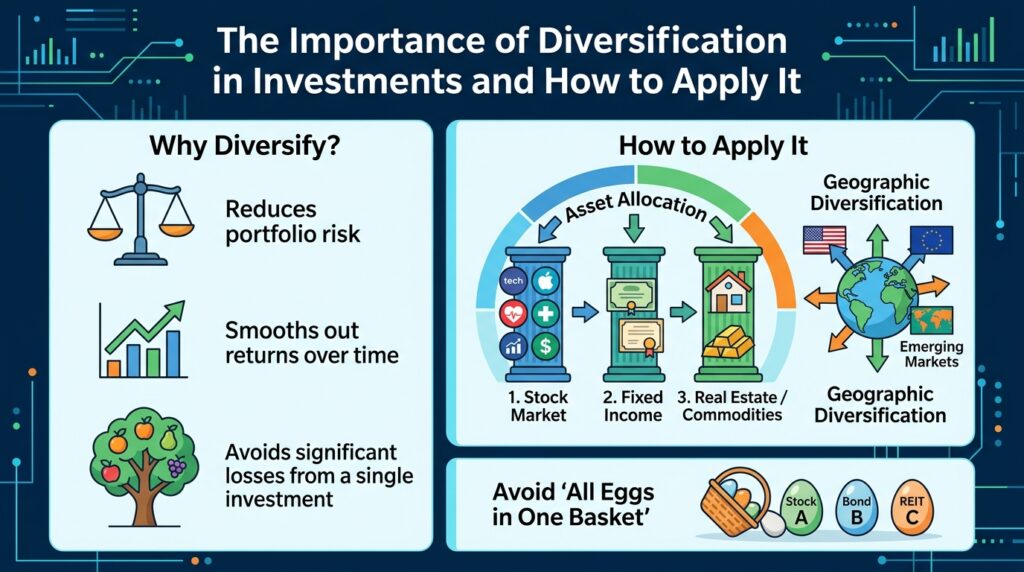

Diversifying Across Asset Classes

The most fundamental layer of diversification happens across asset classes, stocks, bonds, real estate, cash, and alternative investments like commodities or precious metals. Each of these categories tends to respond differently to economic conditions. When stocks fall during a recession, bonds often hold steady or even rise, providing a cushion for your overall portfolio.

This doesn’t mean you need to own every single asset class to be diversified. Rather, it means understanding how the assets you do own behave relative to each other, and intentionally including categories that respond differently to the same economic events. A portfolio entirely made up of stocks, even if spread across many different companies, is still vulnerable to broad market downturns affecting all stocks simultaneously.

- Stocks: growth potential, but higher volatility and sensitivity to economic cycles

- Bonds: generally more stable, often move inversely to stocks during downturns

- Real estate: tends to have lower correlation with stock markets, though not immune to economic shifts

- Cash and cash equivalents: provides stability and liquidity, though minimal growth

- Commodities: can act as a hedge against inflation, often moving independently of stocks and bonds

Diversifying Within Asset Classes: The Often-Missed Layer

Once you’ve diversified across asset classes, the next layer involves diversifying within each class. For stocks, this means spreading investments across different sectors (technology, healthcare, finance, energy, consumer goods), different company sizes (large-cap, mid-cap, small-cap), and different geographic regions (domestic and international markets).

This is where index funds and ETFs become incredibly valuable tools for Investments and How to Apply It in practice. A single total market index fund might hold thousands of individual stocks across every major sector and company size, instantly providing the kind of internal diversification that would be nearly impossible to achieve by manually selecting individual stocks one by one.

The same principle applies to bonds. Government bonds, corporate bonds, and municipal bonds each carry different risk profiles and respond differently to interest rate changes. A bond fund that holds a mix of these, across different maturities, provides more stability than concentrating in just one type of bond or one specific maturity date.

Geographic Diversification: Looking Beyond Your Home Country

One area that even experienced investors sometimes overlook is geographic diversification. It’s natural to feel most comfortable investing in companies based in your own country, you understand the economy, the news, and the companies themselves. But this familiarity bias can lead to a portfolio that’s overly exposed to a single country’s economic conditions.

Different countries and regions experience economic cycles at different times. While one region might be in a downturn, another could be experiencing growth. Including international exposure in your portfolio, whether through international index funds or specific regional funds, helps smooth out these differences and reduces dependence on any single economy’s performance.

A personal observation worth sharing: many investors who lived through a prolonged downturn in their home market, watching their portfolios stagnate for years while other global markets grew, often wish they had diversified geographically sooner. This is a clear example of why Investments and How to Apply It should include a global perspective, not just a domestic one.

Time Diversification: Spreading Investments Across Different Periods

Diversification isn’t only about what you invest in, it’s also about when you invest. This concept, often called “dollar-cost averaging,” involves investing a fixed amount of money at regular intervals, regardless of whether the market is up or down, rather than trying to time a single “perfect” moment to invest a large lump sum.

The benefit here is psychological as much as financial. Trying to time the market perfectly is notoriously difficult, even for professionals, and the fear of “buying at the wrong time” causes many people to delay investing altogether, sometimes for years, missing out on growth in the meantime. By spreading purchases over time, you naturally buy more shares when prices are low and fewer when prices are high, averaging out your cost basis.

- Set up automatic monthly or biweekly contributions to your investment accounts

- Avoid the temptation to pause contributions during market downturns, when shares are effectively “on sale”

- Resist the urge to invest large lump sums all at once if it causes significant anxiety

- Stay consistent regardless of short-term market news or headlines

How Much Diversification Is Actually Enough

It’s possible to take diversification too far, a phenomenon sometimes called “over-diversification.” If you own so many overlapping funds that you essentially own the entire market multiple times over through different products, you’re not gaining additional protection, you’re just adding complexity and potentially higher fees without meaningful benefit.

A genuinely diversified portfolio doesn’t need to be complicated. Often, a handful of broad, low-cost funds covering domestic stocks, international stocks, and bonds can provide exposure to thousands of underlying securities across the globe. Adding ten more funds on top of this often results in significant overlap rather than meaningfully improved diversification.

The key question to ask isn’t “how many investments do I own?” but rather “if one of these investments performed terribly, how much would it actually affect my overall portfolio?” If the answer is “barely at all,” you’re likely well-diversified, even if your portfolio consists of just a few well-chosen funds.

Rebalancing as an Ongoing Diversification Tool

Diversification isn’t a one-time setup, it requires occasional maintenance through rebalancing. Over time, some investments will grow faster than others, gradually shifting your portfolio’s actual allocation away from your intended diversification strategy, even if you never made an active decision to change it.

For example, if stocks have a strong year while bonds remain flat, your portfolio might drift from an intended 70/30 stock-to-bond split toward 80/20, increasing your overall risk exposure without any deliberate choice on your part. Periodically rebalancing back to your target allocation maintains the diversification balance you originally established.

For those wanting to dig deeper into portfolio construction and rebalancing strategies, Investor.

gov offers free educational resources on asset allocation, while Bogleheads.

org hosts an active community discussion forum where investors share practical experiences with diversification strategies across different life stages.

Common Diversification Mistakes to Avoid

Even with good intentions, certain habits can undermine diversification efforts without investors realizing it. Being aware of these patterns can help you build a portfolio that’s genuinely protected rather than just appearing diversified on paper.

- Owning multiple funds that hold largely the same underlying companies, creating false diversification

- Concentrating heavily in your employer’s stock through workplace retirement plans

- Ignoring international markets entirely due to home-country familiarity bias

- Treating diversification as a one-time task rather than an ongoing process requiring rebalancing

- Confusing the number of holdings with actual diversification quality

The common thread among these mistakes is a surface-level understanding of diversification that doesn’t account for correlation, overlap, or genuine risk reduction. Truly mastering Investments and How to Apply It requires looking beneath the surface of your portfolio, not just counting how many different things you own.

Putting Diversification Into Practice Today

If you’re starting from scratch or reviewing an existing portfolio, a practical first step is mapping out what you currently own and identifying any obvious gaps or overlaps. Are you heavily concentrated in one sector? Do you have any international exposure? Is your bond allocation appropriate for your timeline and risk tolerance?

From there, broad, low-cost index funds covering domestic stocks, international stocks, and bonds provide a solid foundation that addresses most diversification needs without unnecessary complexity. Additional diversification, into real estate, commodities, or alternative assets, can be layered in gradually as your portfolio grows and your understanding deepens.

Remember that diversification doesn’t eliminate risk entirely, and it doesn’t guarantee profits. What it does is reduce the impact of any single investment’s poor performance on your overall financial wellbeing, allowing you to participate in long-term growth while sleeping a little better at night, even when individual investments have rough periods.

Final Thoughts on Building a Resilient Portfolio

Diversification is often described as the only “free lunch” in investing, a way to reduce risk without necessarily sacrificing expected returns. While that might be a slight oversimplification, the core idea holds true: spreading your investments thoughtfully across different assets, sectors, and regions genuinely improves your portfolio’s resilience against unpredictable events.

Understanding Investments and How to Apply It isn’t about memorizing a checklist, it’s about developing an instinct for asking “what happens to my portfolio if this specific thing goes wrong?” and ensuring the answer is never “everything falls apart.” That mindset, more than any specific fund or strategy, is what genuine diversification provides.

Have you ever discovered hidden concentration in your own portfolio that surprised you? Do you currently include international investments, or has home-country bias kept you closer to familiar markets? Share your experiences, questions, or even diversification “aha moments” in the comments below, these real-world stories often help other readers more than abstract advice ever could.

Frequently Asked Questions

Is it possible to be too diversified?

Yes, owning too many overlapping funds can add complexity and fees without meaningfully improving risk protection, sometimes called over-diversification.

Do I need international investments to be properly diversified?

While not strictly required, international exposure helps reduce dependence on a single country’s economic performance and is generally considered a valuable diversification component.

How often should I check my portfolio for concentration risk?

Reviewing your portfolio once or twice a year is generally sufficient, particularly checking for employer stock concentration and any single positions that have grown disproportionately large.

Can index funds alone provide enough diversification?

A combination of broad domestic, international, and bond index funds can provide substantial diversification across thousands of securities with just a few funds.

Does diversification guarantee I won’t lose money?

No, diversification reduces risk but doesn’t eliminate it entirely. Broad market downturns can still affect diversified portfolios, though typically less severely than concentrated ones.

Michael Rowan is a dedicated writer and researcher specializing in Personal Finance and Investments. With a passion for helping individuals make smarter financial decisions, he creates informative and practical content designed to simplify complex financial topics.