How to Build the Habit of Saving Money Every Month

|

Getting your Trinity Audio player ready...

|

Most people don’t struggle to save money because they lack willpower, they struggle because saving feels like an event rather than a habit. One month you save a little, the next month an unexpected expense wipes it out, and by the third month you’ve given up entirely. The real goal isn’t a single impressive deposit, it’s learning how to save money every month, consistently, even when life throws curveballs your way.

This article isn’t going to tell you to stop buying coffee or cancel every subscription you enjoy. Instead, we’ll dig into the psychology and systems behind building a habit that sticks, why most people fail at it, and practical, slightly unconventional strategies that actually make it easier to save money every month without feeling like you’re constantly depriving yourself.

Why Saving Money Every Month Feels So Hard

If saving were purely about math, everyone would do it effortlessly. The problem is that saving money competes directly with immediate gratification, and our brains are wired to prioritize “now” over “later,” even when we logically know the future matters. This is why New Year’s resolutions to save more often fizzle out by February.

Another major issue is that most people try to save with whatever is “left over” at the end of the month. But there’s rarely anything left over, expenses have a sneaky way of expanding to fill whatever income is available. If you want to genuinely save money every month, the approach needs to flip: saving has to happen first, not last, treated as a non-negotiable expense rather than an optional afterthought.

The Pay-Yourself-First Principle in Practice

“Pay yourself first” is a phrase you’ve probably heard before, but understanding why it works is more important than just nodding along. When you set aside savings the moment income arrives, before paying bills, before grocery shopping, before anything else, you remove the decision-making process entirely. The money is gone from your spending account before you even have a chance to mentally allocate it elsewhere.

This works because of a psychological quirk: people adapt their spending to whatever amount of money is visibly available to them. If $500 disappears into savings the moment you’re paid, your brain adjusts and starts planning around the remaining amount as if that’s simply what you have. Most people are surprised at how quickly this adjustment happens, often within just a month or two.

- Set up an automatic transfer to a separate savings account on payday

- Choose an amount that feels slightly uncomfortable, but not impossible

- Keep this savings account at a different bank to reduce the temptation to transfer money back

- Increase the automated amount gradually every few months as your income or comfort grows

Starting Small: Why Tiny Amounts Actually Matter

One of the biggest myths about saving is that it’s only worthwhile if you’re putting away large amounts. This belief actually prevents many people from starting at all, they wait until they’re earning more, until expenses decrease, until some imagined “better time” arrives. That better time rarely comes on its own.

The truth is that the habit matters more than the amount, at least initially. Someone who manages to save money every month, even just $20 or $30, is building a behavioral pattern, a mental association between receiving income and setting some aside automatically. Once that pattern is established, increasing the amount becomes far easier than starting the habit from zero with a large target.

Think of it like exercise. Someone who has never worked out is far more likely to succeed by committing to ten minutes of walking daily than by attempting an hour-long intense gym session they’ll dread and eventually skip. The same logic applies to saving: small, consistent actions build the foundation for larger ones later.

Tracking Spending Without Becoming Obsessive

There’s a balance between being aware of where your money goes and becoming so obsessed with tracking every penny that the process itself becomes exhausting and unsustainable. The goal of tracking spending isn’t perfection, it’s awareness, identifying patterns you might not have noticed otherwise.

Many people are genuinely surprised when they review a month of spending broken down by category. Subscriptions they forgot about, food delivery costs that add up faster than expected, or small recurring charges that seemed insignificant individually but represent a meaningful chunk of money collectively. This awareness alone often naturally reduces unnecessary spending, without requiring strict budgeting rules.

- Review bank and credit card statements at least once a month, categorizing expenses broadly

- Look specifically for forgotten subscriptions or recurring charges

- Identify one or two categories where spending feels disproportionate to the value received

- Avoid tracking every single transaction in real-time if it feels overwhelming, monthly reviews are often enough

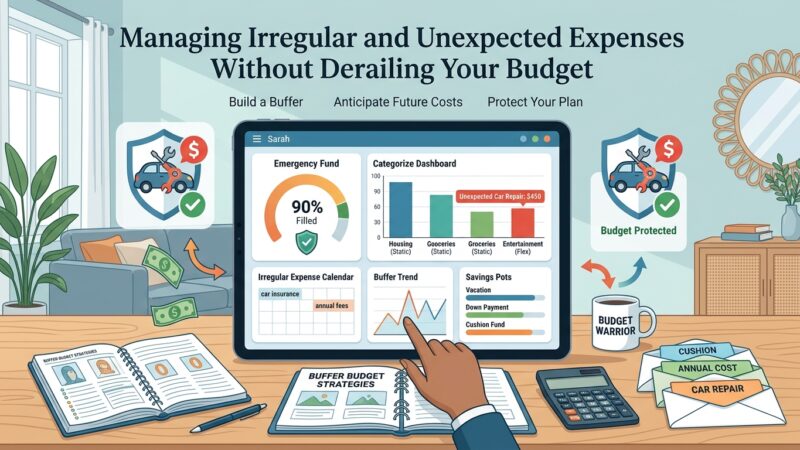

Dealing With Irregular Income and Unexpected Expenses

For people with variable income, freelancers, commission-based workers, or anyone whose paycheck fluctuates, the standard advice to automate a fixed monthly transfer can feel impossible. How do you commit to a set amount when you genuinely don’t know what next month’s income will look like?

One practical approach is saving based on percentages rather than fixed amounts. Instead of committing to save $200 every month regardless of circumstances, commit to saving 10% (or whatever percentage feels realistic) of whatever comes in, whenever it comes in. This scales naturally with fluctuating income, allowing you to save money every month even when “every month” looks financially different from the last.

For unexpected expenses, the real solution isn’t trying to predict every possible scenario, it’s having a buffer specifically designed to absorb them. This is different from your regular savings goal; it’s a separate cushion that exists precisely so that an unexpected car repair or medical bill doesn’t derail your monthly saving habit entirely.

Creating Visual Reminders and Milestones

Humans respond well to visual progress. Watching a number grow, whether it’s a savings account balance, a progress bar, or even a simple spreadsheet, provides a psychological reward that pure numbers in a bank statement often fail to deliver. This is part of why some people use separate accounts or even physical methods for different savings goals.

Breaking a larger goal into smaller milestones can also make the process feel less abstract. Instead of “save $6,000 this year,” which can feel distant and overwhelming, framing it as “save $500 this month” makes the goal immediate and achievable, while still adding up to the same yearly total. Each monthly success becomes its own small win worth acknowledging.

A personal observation: many people find that celebrating small milestones, not with spending, but with simple acknowledgment, checking off a goal, updating a tracker, telling a friend, helps reinforce the habit far more than waiting silently for some distant final number to be reached.

Handling Social Pressure and Lifestyle Inflation

One of the sneakiest obstacles to saving consistently isn’t a single big expense, it’s the gradual creep of lifestyle inflation. As income increases, spending often increases right alongside it, sometimes even faster, leaving the percentage actually saved unchanged or even reduced, despite earning more than before.

Social pressure plays a role here too. Friends upgrading their cars, colleagues talking about vacations, family expectations around gifts or celebrations, all of these create subtle pressure to spend in ways that align with social circles, even when it conflicts with personal financial goals. Recognizing this pressure for what it is, rather than internalizing it as “normal” spending, is an important step toward consistency.

This doesn’t mean never enjoying lifestyle improvements as income grows. It means being intentional about which improvements genuinely add value to your life versus which ones are simply responses to external expectations. Someone who consciously decides to save money every month despite income growth, by maintaining or only gradually increasing their lifestyle, builds wealth significantly faster than someone whose spending mirrors their income increases dollar for dollar.

Using Technology to Make Saving Effortless

Modern banking and financial apps have made automating savings easier than ever before. Beyond simple automatic transfers, many apps now offer features like “round-up” savings, where everyday purchases are rounded to the nearest dollar and the difference is automatically saved, turning routine spending into passive saving without any active effort.

Other apps analyze spending patterns and suggest “safe to save” amounts based on upcoming bills and typical spending, automatically transferring small amounts when your account has more than usual. While these tools shouldn’t replace a deliberate savings plan, they can complement it, capturing small amounts that might otherwise go unnoticed and unused.

For those wanting to explore budgeting tools further, resources like ConsumerFinance.

gov offer free guidance on building budgets and savings plans, while apps like NerdWallet provide comparisons of savings accounts with competitive interest rates, helping your saved money grow a little faster while it sits.

What to Do When You Miss a Month

Despite the best intentions, there will be months where saving simply isn’t possible, an emergency arises, income drops, or unexpected expenses consume what would have been saved. This is normal, and how you respond to these moments matters far more than the missed month itself.

The biggest risk after missing a month isn’t the missed contribution, it’s the psychological spiral that sometimes follows: “I already broke the habit, so what’s the point of continuing?” This all-or-nothing thinking can turn a single missed month into a permanently abandoned habit. The healthier response is simply resuming the next month as if nothing happened, without guilt, without trying to “catch up” by saving double, which often creates additional stress.

- Treat a missed month as an exception, not evidence that the habit has failed

- Resume automatic transfers immediately the following month

- Avoid the temptation to “punish” yourself with unrealistic catch-up amounts

- Reflect briefly on what caused the gap, without dwelling on it excessively

Final Thoughts on Making Saving a Lasting Habit

Building the habit to save money every month isn’t about finding one perfect strategy and rigidly sticking to it forever. It’s about experimenting with different approaches, automation, percentage-based saving, visual tracking, until you find a system that fits naturally into your life rather than fighting against it constantly.

The compounding effect of consistent monthly saving, even in modest amounts, often surprises people when they look back after a year or two. What felt like a small, almost insignificant habit in month one becomes a meaningful financial cushion, and eventually, a foundation for larger financial goals like investing, paying off debt, or handling emergencies without stress.

What’s your experience been with saving consistently? Have you found a specific trick, app, or system that finally made it click for you? Or are you still searching for an approach that fits your lifestyle? Share your stories, struggles, or tips in the comments below, sometimes the most useful advice comes from people who’ve been exactly where you are.

Frequently Asked Questions

How much should I be saving each month?

There’s no universal number, but a common starting point is aiming for 10-20% of income, though even smaller amounts are valuable when starting out, the habit matters more than the percentage initially.

What if my income changes every month?

Consider saving a percentage of income rather than a fixed amount, this naturally scales with fluctuations and still allows you to save money every month regardless of how much comes in.

Is automating savings really more effective than manual saving?

Yes, automation removes the need for willpower and decision-making each month, which is often the biggest barrier to consistency for most people.

What should I do if I miss a month of saving?

Simply resume the following month without trying to “catch up” with unrealistic amounts. Treat it as a normal exception rather than a failure of the entire habit.

Should I save before or after paying bills?

Ideally, saving should happen first, immediately when income arrives, before other expenses are paid. This “pay yourself first” approach tends to be far more effective long-term.

Michael Rowan is a dedicated writer and researcher specializing in Personal Finance and Investments. With a passion for helping individuals make smarter financial decisions, he creates informative and practical content designed to simplify complex financial topics.