How to Avoid Impulse Buying and Save More Money: A Practical Guide That Actually Works

|

Getting your Trinity Audio player ready...

|

Let’s be honest — we’ve all been there. You walk into a store to buy one thing and walk out with a bag full of stuff you didn’t plan to get. Or you’re scrolling through an online shop at midnight and suddenly your cart has fifteen items in it.

Impulse buying and saving more money are two concepts that are constantly at war with each other, and understanding that tension is the first step to winning the battle. This guide isn’t about making you feel guilty for your spending habits. It’s about giving you real, tested strategies to take back control of your finances without turning into a miserly hermit.

The truth is that impulse buying and saving more money rarely coexist peacefully. Every unplanned purchase chips away at your financial goals, whether that’s building an emergency fund, paying off debt, or saving for a vacation. And the tricky part? The retail industry spends billions of dollars every year specifically to make you spend without thinking.

You’re not weak — you’re up against an incredibly sophisticated machine. The good news is that once you understand how it works, you can start outsmarting it.

Understanding the Psychology Behind Impulse Buying and Saving More Money

Before you can fix a problem, you need to understand it. Impulse buying is rarely about the product itself — it’s almost always about how you’re feeling in the moment. Marketers and behavioral economists have spent decades studying what triggers unplanned purchases, and the findings are fascinating.

Emotional states like stress, boredom, loneliness, and even excitement are among the most powerful drivers of impulsive spending. That’s why the phrase “retail therapy” exists — shopping gives you a temporary emotional boost, a hit of dopamine that feels great for about twenty minutes and then leaves you with buyer’s remorse.

There’s also a psychological concept called present bias, which means our brains are wired to value immediate rewards far more than future ones. When you’re standing in front of a shiny new gadget, the pleasure of owning it right now feels much more real than the abstract benefit of having that money in your savings account six months from now. Understanding this bias doesn’t make you immune to it, but it does give you a powerful tool: awareness.

The moment you recognize that your brain is prioritizing the short-term, you can pause and ask yourself whether the long-term reward is worth more.

Another factor is the scarcity principle. When you see a tag that says “Only 3 left in stock!” or “Sale ends tonight!”, your brain perceives a threat of missing out. This is a manufactured sense of urgency designed to short-circuit your rational thinking.

Once you start recognizing these tactics — urgency timers, limited-time offers, “buy one get one” deals — they lose a significant amount of their power over you. Knowledge truly is financial power here.

Practical Strategies to Avoid Impulse Purchases Every Day

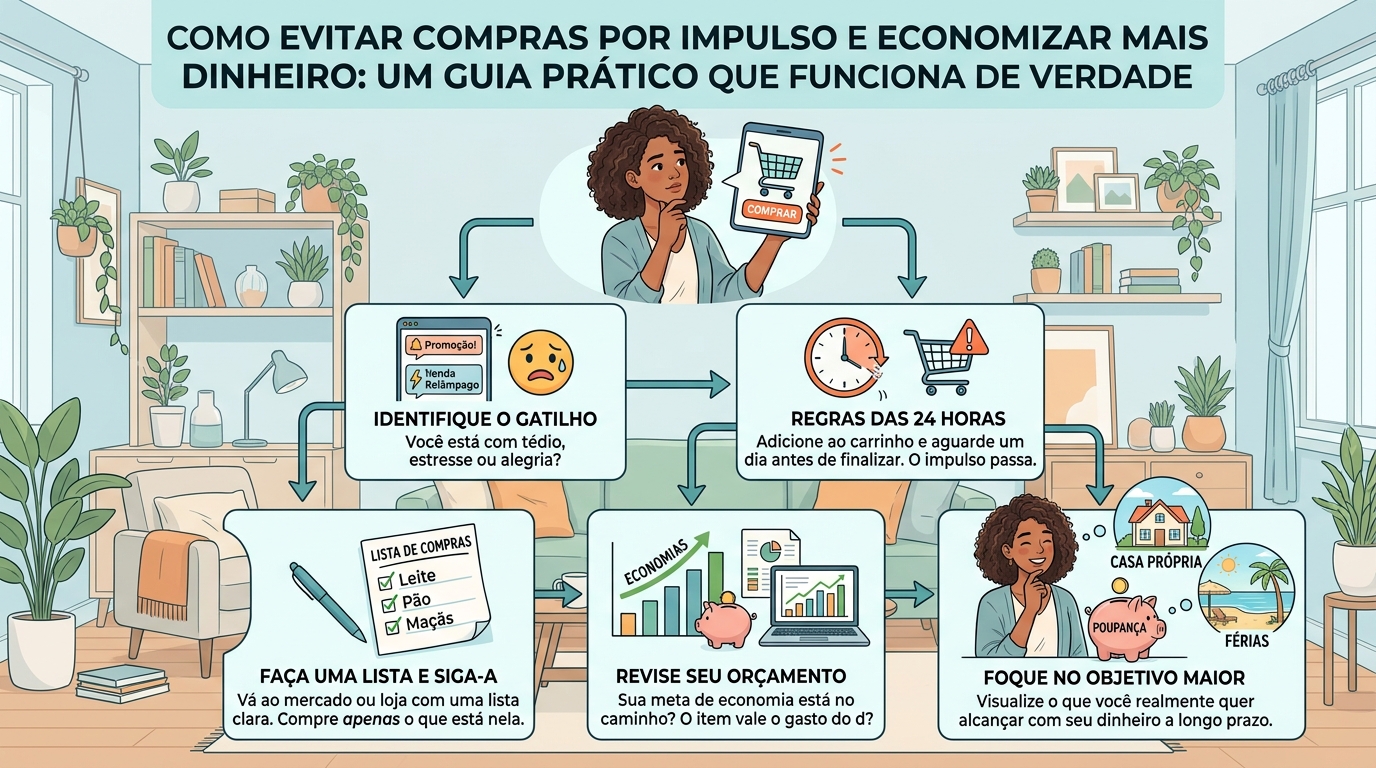

One of the most effective tools in fighting impulse buying and saving more money is the simple act of making a list — and actually sticking to it. Whether you’re heading to the grocery store, the mall, or an online marketplace, going in with a clear and specific list of what you need creates a psychological boundary. It shifts your mindset from browsing mode to mission mode.

Every item that’s not on the list gets mentally flagged as a potential impulse purchase, and that flag alone is often enough to make you pause.

The 24-hour rule is another strategy that works remarkably well. Whenever you feel the urge to buy something that wasn’t planned, you simply wait 24 hours before making the purchase. In most cases, you’ll find that the desire fades significantly — or disappears entirely.

If you still want the item after a full day has passed, then it might be a genuine need or a purchase that genuinely brings value to your life. If you’ve already forgotten about it, you just saved yourself some money. For bigger purchases, consider extending this to a 48- or 72-hour rule.

Unsubscribing from retail email newsletters and promotional alerts is a step many people overlook, but it makes a massive difference. When you’re not being constantly reminded of sales, new arrivals, and exclusive deals, you simply don’t think about shopping as often. Out of sight really does mean out of mind when it comes to consumer temptation.

Take thirty minutes one afternoon to go through your inbox and unsubscribe from every store newsletter. Your wallet will thank you within weeks.

- Delete saved payment information from online stores — the extra friction of having to re-enter your card number is often enough to stop an impulse buy.

- Avoid shopping when hungry, tired, or emotionally drained — these states dramatically lower your impulse control.

- Use browser extensions like Honey or Capital One Shopping to compare prices, which slows down the purchasing process and encourages reflection.

- Set spending limits on your banking app or credit card for categories like dining, entertainment, and clothing.

- Keep your phone out of reach when watching TV or during downtime — idle scrolling frequently leads to unplanned purchases.

Building a Budget That Actually Supports Your Financial Goals

Budgeting often gets a bad reputation as being restrictive or complicated, but a well-designed budget is actually one of the most liberating tools you can have. When you know exactly where your money is going, you stop feeling vague anxiety about your finances and start feeling genuine control. The key to building a budget that works — especially one that helps you fight impulse buying and save more money — is to make it realistic rather than aspirational.

A budget that’s too tight will make you feel deprived, which ironically leads to more impulsive spending as a form of emotional rebellion.

The 50/30/20 rule is a popular framework that’s beginner-friendly and effective. The idea is that 50% of your after-tax income goes toward needs (rent, utilities, groceries, transportation), 30% goes toward wants (dining out, entertainment, hobbies), and 20% goes toward savings and debt repayment. The beauty of this system is that it gives you guilt-free permission to enjoy your life within boundaries, while also ensuring that your future self is being taken care of.

You’re not denying yourself anything — you’re just being intentional about it.

Another approach that’s gained a lot of traction in personal finance communities is the zero-based budget, where every single dollar of your income is assigned a specific job before the month begins. This might sound extreme, but it actually gives you an incredibly clear picture of your financial life and leaves zero room for unplanned spending to sneak in unnoticed. Apps like YNAB (You Need A Budget) make this process much easier and more intuitive than it sounds.

When every dollar has a name and a purpose, impulse purchases become much harder to justify — because you can see in real time exactly what they’re costing you.

Smart Shopping Habits That Help You Save More Money Long-Term

Avoiding impulse buying and saving more money isn’t just about restraint — it’s also about shopping smarter when you do make purchases. One of the best habits you can develop is buying quality over quantity. It’s tempting to go for the cheaper option when you’re trying to save, but frequently buying low-quality items that wear out quickly ends up costing more over time than investing in something durable from the start.

This is sometimes called the “cost per use” framework: divide the price of an item by how many times you’ll realistically use it to get its true cost.

Meal planning is one of the most underrated money-saving strategies available to anyone. When you plan your meals for the week before you go grocery shopping, you buy exactly what you need and nothing more. This eliminates the impulse purchases that come from wandering the grocery aisles without a plan, and it also dramatically reduces food waste.

Studies consistently show that the average household wastes a significant percentage of the food it buys — and every piece of food you throw away is money you might as well have thrown directly in the trash.

Consider embracing a shopping moratorium for certain categories for a set period of time. This is popular in communities like r/BuyItForLife and No Buy forums on Reddit, where people challenge themselves to buy nothing new in a specific category — clothes, books, electronics — for a month or more. These challenges are eye-opening because they force you to confront how much of your buying was habitual rather than necessary.

And more often than not, people discover they’re perfectly happy without the things they were buying on autopilot.

- Shop with cash when possible — physically handing over money makes spending feel more real than swiping a card.

- Buy secondhand for categories like clothing, furniture, and electronics — you can get excellent quality at a fraction of the price.

- Use cashback apps like Rakuten or Ibotta for purchases you were already going to make.

- Compare unit prices at the grocery store, not just package prices — the bigger pack isn’t always the better deal.

- Shop alone when you can — friends and family can influence you to spend more than you planned.

How to Rewire Your Relationship With Money and Spending

Here’s something that most financial advice articles won’t tell you: lasting change in your spending habits requires working on your relationship with money itself, not just following a set of rules. If you grew up in a household where money was scarce, you might subconsciously spend impulsively as a way of rebelling against that scarcity, or conversely, you might hoard money anxiously without ever enjoying it. If you grew up watching adults shop recreationally, you might have internalized shopping as a normal way to spend free time.

These patterns run deep, and acknowledging them is a crucial part of making sustainable change.

Journaling about your spending is a surprisingly powerful tool. After any purchase — planned or impulsive — take a moment to write down how you were feeling before you bought it, during the purchase, and afterward. Over time, patterns will emerge.

You might notice that you tend to make impulse purchases after stressful workdays, or on weekends when you’re bored. Once you can see those triggers clearly, you can start creating alternative responses to them. Instead of shopping when you’re stressed, you might go for a walk, call a friend, or cook something you enjoy.

Building a savings habit is also about making saving feel rewarding, not punishing. One way to do this is to set up a dedicated savings account with a specific goal attached to it — a trip to Portugal, a new camera, a down payment on a car. When your savings account is tied to something meaningful and exciting, contributing to it feels like a reward rather than a deprivation.

Automate your savings transfers so the money moves before you have a chance to spend it, and watch the number grow with the same pleasure you might otherwise get from shopping.

The Role of Environment in Controlling Impulse Buying and Saving More Money

Your environment plays a much larger role in your spending behavior than most people realize. The principle of environmental design — which comes from behavioral economics — suggests that the easiest way to change a behavior is to change the environment in which that behavior occurs, rather than relying purely on willpower. Willpower is a finite resource that gets depleted throughout the day, especially when you’re tired, hungry, or stressed.

But a well-designed environment works for you automatically, without requiring mental effort every time.

In practical terms, this means making impulse buying harder and saving easier. Remove shopping apps from your phone’s home screen. Log out of your online shopping accounts so that purchasing requires multiple extra steps.

Keep your credit cards in a drawer at home instead of in your wallet. On the flip side, make saving easier: set up automatic transfers to your savings account on payday, keep a visual tracker of your financial goals somewhere you’ll see it daily, and surround yourself with people who share your financial values. Your social environment matters too — if everyone around you is constantly talking about their latest purchases, it normalizes and encourages similar behavior in you.

Think carefully about how you spend your leisure time. If browsing online stores or walking through malls is your primary form of entertainment, you’re setting yourself up for frequent temptation. Finding hobbies and activities that don’t revolve around purchasing — hiking, reading, cooking, volunteering, learning an instrument — not only protects your wallet but also tends to bring deeper and more lasting satisfaction than shopping does.

You’re replacing a shallow reward loop with meaningful engagement, which is a genuinely better deal for your wellbeing as well as your bank account.

Using Technology Wisely to Support Your Savings Goals

Technology is a double-edged sword when it comes to impulse buying and saving more money. On one hand, targeted advertising, one-click purchasing, and app notifications are specifically designed to make you spend. On the other hand, there are genuinely excellent tools available that can help you track, manage, and optimize your finances in ways that previous generations could only dream of.

The key is to be intentional about which technologies you allow into your financial life.

Budgeting apps like Mint, YNAB, PocketGuard, and Goodbudget can give you a real-time picture of your spending that would have required hours of manual work just a generation ago. When you can see at a glance that you’ve spent 80% of your dining budget by the third week of the month, it creates a natural stopping point that’s far more effective than vague intentions. Many of these apps also send you alerts when you’re approaching your limits, which brings conscious awareness to what might otherwise be automatic behavior.

Price tracking tools like CamelCamelCamel (for Amazon prices) or the Honey browser extension can help you verify whether a “sale” price is actually a good deal or just clever marketing. It’s remarkably common for retailers to artificially inflate the “original” price of items before putting them “on sale,” creating the illusion of a bargain where none actually exists. Being able to see a product’s price history instantly deflates that illusion and helps you make purchasing decisions based on real value rather than manufactured urgency.

Teaching Yourself and Your Family to Build Lasting Financial Resilience

If you have children or a partner, the habits and conversations you have around money at home have a profound impact on everyone’s financial future. Children who grow up in households where money is discussed openly, where needs and wants are distinguished clearly, and where saving is celebrated tend to become financially healthier adults. This doesn’t mean lecturing your kids about money at every opportunity — it means modeling the behavior you want to see and having age-appropriate conversations about why your family makes the financial choices it does.

With a partner, financial alignment is one of the most important — and often most challenging — aspects of a shared life. Couples who have different spending styles or different levels of financial literacy frequently find that money becomes a source of significant conflict. Regular “money dates” — a designated time each week or month to review your finances together, celebrate progress, and adjust your plans — can transform money from a source of stress into a shared project you’re both working on.

Approaching finances as a team, rather than as adversaries, makes it much easier to hold each other accountable without it feeling like judgment or control.

Ultimately, the goal of all these strategies is not to make you into someone who never enjoys spending money. It’s to make sure that when you do spend money, it’s genuinely aligned with what you care about and what makes your life better. Impulse buying and saving more money don’t have to be constant points of tension in your life.

With the right systems, habits, and mindset, they become manageable — and eventually, saving starts to feel just as satisfying as spending ever did. That’s when you know you’ve genuinely changed your relationship with money, and that’s when the real financial freedom begins.

Frequently Asked Questions About Impulse Buying and Saving More Money

What is the main cause of impulse buying?

Impulse buying is most commonly driven by emotional triggers such as stress, boredom, excitement, or social influence. Retailers also use marketing tactics like limited-time offers and strategic product placement to encourage unplanned purchases. Understanding your personal triggers is the first step toward controlling them.

How much money can I save by cutting out impulse purchases?

This varies widely by individual, but studies suggest the average person spends hundreds to over a thousand dollars per year on unplanned purchases. Even reducing impulse spending by 50% can free up significant funds for savings goals, debt repayment, or meaningful experiences.

Does the 24-hour rule really work?

Yes, for many people it’s highly effective. Research on consumer behavior consistently shows that the desire to purchase impulsively diminishes significantly when there’s a delay between the urge and the action. Most people find that 70–80% of impulse purchase urges fade within 24 hours.

Is it okay to sometimes buy things impulsively?

Absolutely. The goal isn’t to eliminate all spontaneous spending — it’s to make sure it’s the exception rather than the rule, and that it’s within a budget you can sustain. Occasional unplanned purchases that bring genuine joy are perfectly healthy.

Problems arise when impulse buying becomes habitual and undermines your financial goals.

What budgeting method works best for avoiding impulse spending?

There’s no one-size-fits-all answer, but zero-based budgeting and the envelope method tend to be the most effective for people who struggle with impulse control, because they require you to assign a specific purpose to every dollar before you spend it. Digital tools like YNAB make these methods much easier to implement than they used to be.

How can I make saving money feel more rewarding?

Tie your savings goals to something specific and meaningful — a trip, a major purchase, financial independence. Use visual trackers to see your progress. Celebrate milestones.

Automate your savings so you build momentum without relying on willpower. The more tangible and exciting your goal, the more motivating saving becomes.

What strategies have you found most effective for resisting impulse purchases? Have you tried a no-buy challenge, the 24-hour rule, or a budgeting app that changed your habits? Share your experiences and tips in the comments below — your insights might be exactly what someone else needs to hear to start their own journey toward financial freedom.

Michael Rowan is a dedicated writer and researcher specializing in Personal Finance and Investments. With a passion for helping individuals make smarter financial decisions, he creates informative and practical content designed to simplify complex financial topics.