Family Financial Planning: How to Organize Your Household Bills and Build a Stronger Future Together

|

Getting your Trinity Audio player ready...

|

Managing money as a family is one of the most important — and most challenging — responsibilities that comes with running a household. Whether you’re a couple just starting out, a growing family juggling school expenses and mortgage payments, or empty nesters trying to simplify your finances, knowing how to organize your household bills is the foundation of everything else. Without that foundation, even a good income can feel like it’s never quite enough, because money without structure has a way of disappearing before you can figure out where it went.

The good news is that how to organize your household bills doesn’t have to be complicated or time-consuming. With the right systems in place, you can go from financial chaos to financial clarity in a matter of weeks. This article is going to walk you through every major aspect of family financial planning — from understanding your true income to building an emergency fund, from having productive money conversations with your partner to teaching your kids about financial responsibility.

By the end, you’ll have a clear, actionable roadmap for creating a household financial system that actually works.

Why Most Families Struggle to Organize Their Household Finances

Before we get into solutions, it’s worth understanding why so many families find how to organize their household bills so difficult in the first place. The most common reason is that financial management was never explicitly taught to most of us. We grew up watching our parents handle money in whatever way they handled it — sometimes well, sometimes not — and we absorbed those patterns without ever examining them critically.

Then we moved out, started earning our own money, and just kind of improvised from there.

Another major obstacle is that household finances are genuinely more complex than personal finances. When you’re single, you only have to account for your own income, your own spending priorities, and your own financial habits. When you add a partner — and eventually children — you’re suddenly dealing with multiple income streams, competing priorities, different emotional relationships with money, and a significantly higher volume of bills, subscriptions, and expenses to track.

Without a deliberate system, it’s almost impossible to stay on top of all of it.

There’s also the emotional dimension that people rarely talk about. Money is deeply tied to feelings of security, control, love, and self-worth. When couples disagree about spending, it rarely stays purely logical — it quickly becomes about trust, values, and fairness.

Understanding this emotional layer is crucial to building a financial system that the whole family will actually follow, because a budget that causes constant conflict is one that will eventually be abandoned.

The First Step: Getting a Complete and Honest Picture of Your Finances

You can’t learn how to organize your household bills effectively until you know exactly what those bills are. This sounds obvious, but many families are genuinely surprised when they sit down and list every single recurring expense they have. Start with the fixed expenses — the ones that are the same amount every month: rent or mortgage, car payments, insurance premiums, loan repayments, and any fixed subscription services.

Write every single one down with the exact amount and due date.

Then move on to variable expenses — the ones that change month to month: groceries, utilities, fuel, dining out, clothing, entertainment, and personal care. These are trickier to track because they fluctuate, but they’re often where the most financial leakage occurs. Look back through your last three months of bank and credit card statements and calculate an average for each category.

This exercise alone tends to be extremely eye-opening. Most people dramatically underestimate what they spend on food, for example, or on small recurring subscriptions they’ve forgotten about.

Once you have a complete picture of your expenses, compare the total to your household’s net income — the actual take-home amount after taxes, health insurance deductions, and retirement contributions. If your expenses are higher than your income, you have a deficit that needs to be addressed immediately. If your income is higher than your expenses, the gap between them represents your potential for saving and building wealth.

Either way, you now have the real numbers you need to make informed decisions.

How to Organize Your Household Bills With a System That Lasts

One of the most practical and immediately impactful things you can do when learning how to organize your household bills is to create a centralized bill payment system. This means consolidating all your bills into one place where nothing falls through the cracks. There are several approaches to this, and the best one depends on your personal preferences and the complexity of your financial life.

The bill calendar method is simple and highly effective. Create a calendar — physical or digital — that shows every bill’s due date for the entire year. Color-code by category: housing in blue, utilities in green, insurance in red, and so on.

At a glance, you can see what’s due each week and plan your cash flow accordingly. This prevents the common problem of being caught off guard by a quarterly or annual payment you forgot was coming, like a car insurance renewal or a subscription that charges annually.

The dedicated bill-paying account strategy takes this a step further. Open a separate checking account specifically for household bills. Every month, transfer the exact amount needed to cover all your bills into this account, and set up automatic payments from it.

Your main account then holds only your spending money and savings contributions. This separation makes it psychologically and practically much easier to avoid accidentally spending money that’s earmarked for rent or utilities.

- Set up automatic payments for every fixed bill where possible — this eliminates late fees and the mental load of remembering due dates.

- Use a shared digital calendar (Google Calendar works well) so both partners can see upcoming bills and financial events.

- Create a shared folder in Google Drive or Dropbox for all household financial documents — insurance policies, contracts, tax returns, and receipts.

- Audit your subscriptions every six months — cancel any you’re not actively using, and look for cheaper alternatives to the ones you are.

- Set bill payment reminders five days before due dates as a backup to automatic payments, in case of account issues.

Digital tools have made how to organize your household bills dramatically easier than it was even ten years ago. Apps like Mint, YNAB (You Need A Budget), EveryDollar, and Goodbudget allow you to sync all your accounts, categorize your spending automatically, and see your complete financial picture in real time. For families who prefer a more manual approach, a well-designed spreadsheet can do the job just as effectively — and there are dozens of free household budget templates available through Google Sheets.

Building a Family Budget That Everyone Can Actually Follow

A family budget is only as good as the willingness of every household member to follow it. That’s why the process of creating a budget is just as important as the budget itself. If one partner dominates the budget-making process and presents it to the other as a fait accompli, the one who wasn’t involved is far less likely to feel ownership of it or commitment to it.

Build the budget together, from scratch, with both partners’ priorities represented.

The 50/30/20 framework is a popular starting point for family budgeting. It suggests allocating 50% of your after-tax income to needs (housing, utilities, groceries, transportation, insurance), 30% to wants (dining out, entertainment, hobbies, vacations), and 20% to savings and debt repayment. This framework is useful because it’s simple, balanced, and flexible enough to adapt to most household situations.

However, families in high cost-of-living areas may find that housing alone consumes more than 50% of their income, which means adjustments need to be made in the wants category.

Another approach that works particularly well for families is value-based budgeting. Rather than starting with categories and fitting your life into them, you start by identifying your family’s top five financial priorities — what matters most to you as a household. Maybe it’s homeownership, travel, your children’s education, financial independence, or charitable giving.

Once you’ve identified those priorities, you fund them first and let everything else be secondary. This approach tends to create much stronger emotional buy-in because everyone can see that the budget reflects what the family genuinely cares about.

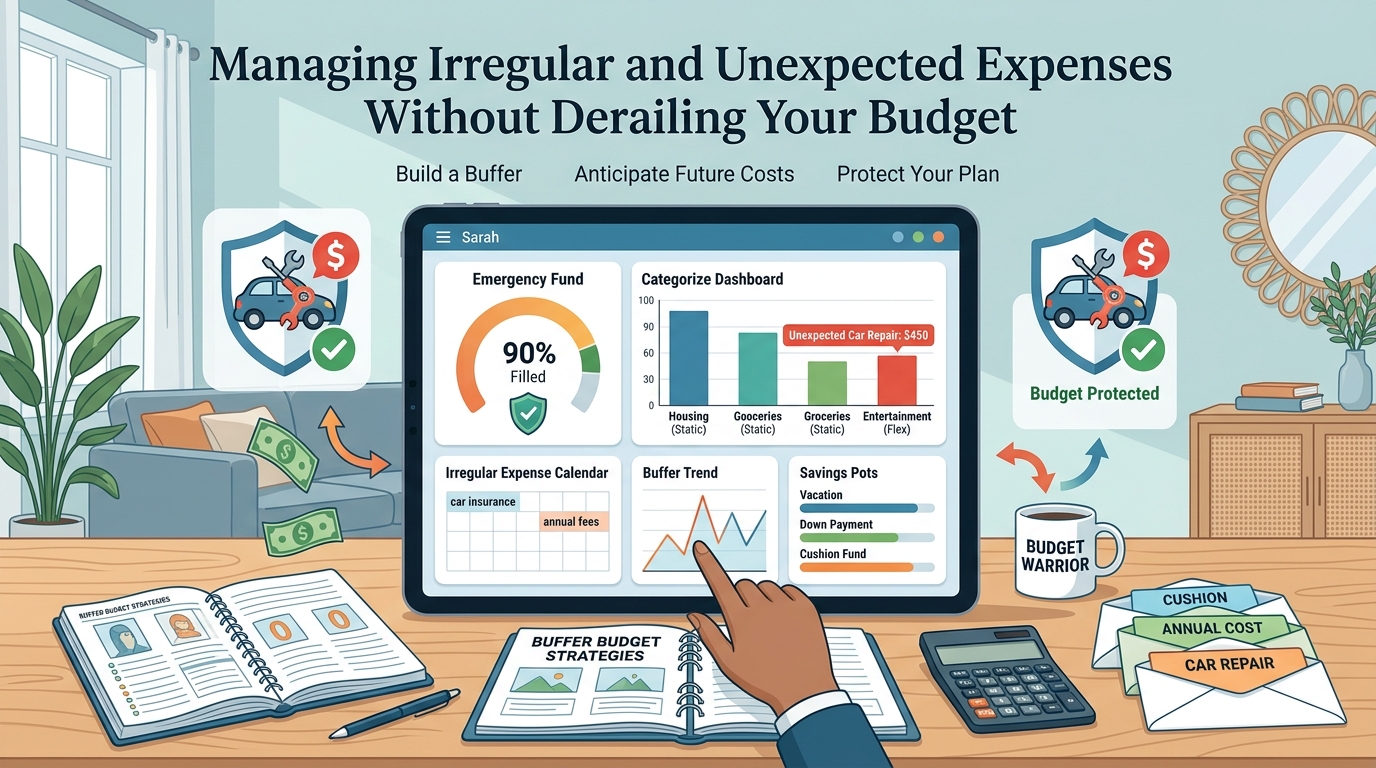

Managing Irregular and Unexpected Expenses Without Derailing Your Budget

One of the biggest reasons household budgets fail is that families only account for predictable monthly expenses and then get derailed by irregular or unexpected costs. Car repairs, medical bills, school fees, home maintenance, holiday gifts, and appliance replacements don’t appear on a regular schedule, but they happen to every family every year. Learning how to organize your household bills properly means accounting for these costs before they occur, not scrambling to deal with them after the fact.

The most effective tool for this is a sinking fund — a dedicated savings bucket for a specific anticipated expense. You calculate the total amount you expect to need, divide it by the number of months until you’ll need it, and set aside that amount each month. For example, if your family typically spends around $1,200 on holiday gifts and travel each December, you’d contribute $100 per month to a holiday sinking fund starting in January.

When December arrives, the money is already there waiting, and your regular budget is completely undisturbed.

Common sinking fund categories for families include:

- Home maintenance and repairs — financial advisors typically recommend setting aside 1–2% of your home’s value annually for maintenance.

- Vehicle maintenance and repairs — oil changes, tires, registration fees, and unexpected repairs add up significantly over a year.

- Medical and dental expenses — even with good insurance, copays, prescriptions, and out-of-pocket costs are inevitable.

- School and childcare costs — back-to-school shopping, field trips, sports fees, and activity costs are easy to underestimate.

- Annual insurance premiums — if you pay any insurance annually rather than monthly, build a sinking fund for it.

- Family vacations — start saving for your next trip as soon as the current one ends.

Beyond sinking funds, every family needs an emergency fund — a completely separate reserve of liquid savings designed to cover truly unexpected crises like job loss, a major medical event, or a sudden essential home repair. Financial experts generally recommend keeping three to six months of essential living expenses in this fund, held in a high-yield savings account where it earns interest but remains accessible. This emergency fund is not a sinking fund — it’s not for planned expenses, no matter how irregular.

It’s a financial safety net that should only be touched in genuine emergencies.

Having Productive Money Conversations as a Family

One of the most transformative things you can do for your family’s financial health has nothing to do with spreadsheets or apps — it’s learning how to talk about money openly, honestly, and without defensiveness. Money conversations in many households are either avoided entirely (because they feel uncomfortable or taboo) or happen only in moments of crisis (when someone overspent or a bill can’t be paid). Neither of these patterns is healthy or productive.

Establishing a regular family money meeting — sometimes called a “budget date” for couples — is a simple practice that can dramatically improve financial communication. Once a week or once a month, set aside 30 to 60 minutes to review your spending from the past period, compare it against your budget, discuss any upcoming financial decisions, and celebrate progress toward your goals. Keep these meetings solution-focused and judgment-free.

The point is to look at the numbers together and make decisions together, not to assign blame or score points.

When conversations do get tense — and sometimes they will — it helps to remember that you and your partner are on the same team. You’re not fighting about money; you’re working together to solve a shared challenge. Approaching spending disagreements with curiosity rather than judgment (“Help me understand why this feels important to you”) tends to lead to much more productive outcomes than accusations or ultimatums.

Many couples find that a session or two with a financial therapist or financial planner can help them establish healthier patterns of financial communication.

Children should be included in age-appropriate financial conversations as well. This doesn’t mean burdening them with adult financial stress, but it does mean letting them see that money requires management and intentionality. Giving children a small allowance and letting them make their own spending decisions — including mistakes — is one of the best financial education tools available.

Talking openly about why your family makes certain financial choices helps children develop values and habits that will serve them for the rest of their lives.

Reducing Household Expenses Without Sacrificing Quality of Life

A key part of mastering how to organize your household bills is identifying where you can reduce expenses without significantly impacting your quality of life. This is different from deprivation — it’s about finding smarter ways to get the same value for less money. And in most households, there’s considerably more room for this than people initially expect.

Start with your largest fixed expenses, because that’s where the biggest savings live. Housing is typically the largest household expense, and while it’s not easily changed in the short term, it’s worth considering whether your current housing costs are sustainable and appropriate for your income. If your rent or mortgage consumes more than 35% of your take-home pay, you’re financially stretched in a way that will make all other financial goals much harder to achieve.

Refinancing your mortgage when rates are favorable, or negotiating your rent at renewal time, can produce significant savings.

Insurance is another area where many families overpay simply because they haven’t shopped around recently. It’s worth getting competing quotes on your home, auto, and life insurance every two to three years. Bundling policies with a single insurer often produces meaningful discounts.

Increasing your deductibles can also lower your premiums significantly — as long as you have the savings to cover the higher deductible if you need to make a claim.

Utility bills are more controllable than most people realize. Simple changes like switching to LED lighting throughout your home, installing a programmable or smart thermostat, fixing leaky faucets, and unplugging electronics when not in use can reduce your monthly utility costs by a meaningful percentage. Many utility companies also offer free energy audits that identify specific opportunities to reduce consumption in your home.

- Review and cancel unused subscriptions — streaming services, gym memberships, magazine subscriptions, and app subscriptions can accumulate quietly into a significant monthly expense.

- Meal plan and cook at home more consistently — this is one of the highest-impact changes most families can make to reduce monthly spending.

- Use the library for books, audiobooks, e-books, movies, and even museum passes — it’s a remarkable free resource that most people underutilize.

- Buy in bulk strategically for non-perishable items you use regularly — but only when you’ve verified the unit price is genuinely lower.

- Negotiate your bills — internet, cable, and phone providers frequently offer better rates to customers who call and ask, especially if you mention a competitor’s pricing.

Setting Long-Term Financial Goals as a Family Unit

Day-to-day bill management is important, but how to organize your household bills is really just the foundation for something much bigger: building long-term financial security and freedom for your entire family. Without long-term goals, short-term sacrifices feel pointless, and it’s much harder to stay motivated when you’re tired or tempted to overspend. Clearly defined goals give your financial system direction and meaning.

Sit down as a family and discuss what you’re working toward. Common long-term financial goals for families include paying off the mortgage early, saving for children’s college education, building enough retirement savings to retire comfortably, starting a family business, or achieving full financial independence — the point at which your investment income covers your living expenses. These goals should be specific (with a target dollar amount and timeline), meaningful to everyone in the household, and challenging but realistic given your income and current financial position.

Once you’ve identified your goals, work backward to determine what monthly contribution is required to reach each one on schedule. This turns abstract aspirations into concrete monthly action items. A family that wants to save $50,000 for a house down payment in five years knows they need to save approximately $833 per month.

That’s a tangible, actionable number that can be built directly into the household budget as a non-negotiable line item — treated with the same seriousness as any other bill.

Investing is a crucial component of long-term family financial planning that many families delay longer than they should because it feels complex or risky. But the earlier you start investing — even modest amounts — the more powerfully compound growth works in your favor. Maximizing contributions to tax-advantaged accounts like 401(k)s and IRAs should be a priority for most families, especially if your employer offers matching contributions.

A fee-only financial planner can help you build an investment strategy that aligns with your family’s specific goals, timeline, and risk tolerance.

Teaching Financial Responsibility to the Next Generation

One of the most lasting gifts you can give your children is a healthy, confident relationship with money. Children who grow up in households where how to organize household bills is treated as a normal, manageable part of adult life — rather than a source of shame, stress, or mystery — are dramatically better prepared for financial independence. And the good news is that you don’t need to be a financial expert to teach your children well.

You just need to be intentional and open.

Age-appropriate financial education starts younger than most parents think. Even a five-year-old can begin to understand the basic concept that money is exchanged for things, that it runs out, and that earning it requires effort. By the time children are in elementary school, they can manage a simple allowance, practice saving toward a goal, and understand the difference between things the family needs and things they want.

Teenagers can be brought into more sophisticated conversations about household budgets, the cost of college, and the basics of investing.

Consider opening a savings account for your child and making regular deposits together a family ritual. Let them watch the balance grow and experience the satisfaction of saving toward something they want. When they’re old enough, introduce them to concepts like interest, compound growth, and the difference between a debit card and a credit card.

These conversations, repeated regularly and embedded in real financial decisions, build financial literacy far more effectively than any classroom curriculum can.

The family financial journey is a long one, and knowing how to organize your household bills is just the beginning. But every sustainable financial future is built on exactly this foundation — clarity about what comes in, intentionality about what goes out, open communication about priorities, and consistent progress toward meaningful goals. Start where you are, use what you have, and take one step at a time.

Financial security is built incrementally, and every good decision you make today is a gift to your future self and your entire family.

Frequently Asked Questions About Family Financial Planning and How to Organize Your Household Bills

How do we start organizing household bills if we’ve never had a system before?

Start by listing every single recurring expense with its amount and due date. Then compare your total expenses to your net monthly income. This gives you a clear baseline.

From there, create a bill calendar, set up automatic payments where possible, and choose a budgeting method that fits your lifestyle. Starting simple is far better than waiting until you can do it perfectly.

How should couples divide financial responsibilities?

There’s no single right answer, but transparency and fairness are non-negotiable. Some couples combine all finances into joint accounts, others maintain separate accounts with a joint account for shared expenses, and others use a hybrid approach. What matters most is that both partners have full visibility into the household finances, both have some personal spending autonomy, and major financial decisions are made together.

How much should a family keep in an emergency fund?

Financial experts generally recommend three to six months of essential living expenses. For families with a single income, variable income, or young children, erring toward six months provides more security. Keep this fund in a high-yield savings account where it’s accessible but not too tempting to dip into for non-emergencies.

What’s the best way to handle financial disagreements between partners?

Approach disagreements as a team problem to solve rather than a debate to win. Schedule regular money meetings so finances are discussed calmly and proactively, not only in moments of crisis. If disagreements are frequent or severe, a session with a financial therapist or couples counselor who specializes in money conflicts can be genuinely transformative.

At what age should children start learning about household finances?

Financial education can start as early as age four or five with simple concepts like saving and spending. By age eight to ten, children can manage a small allowance and practice goal-based saving. Teenagers should have a solid understanding of budgeting, credit, and long-term saving.

The key is making financial conversations a normal, regular part of family life rather than a topic reserved for crises.

How often should we review our household budget?

A monthly review is the minimum recommended frequency for most families. Weekly check-ins are even better for families who are in debt repayment mode or working toward a major financial goal. Your budget should also be reviewed and updated whenever there’s a significant change in income, expenses, or family circumstances.

We’d love to hear from you — what has been your biggest challenge when it comes to organizing your household finances? Have you found a budgeting method, app, or family practice that’s made a real difference? Share your story and tips in the comments below. Your experience could be exactly the insight another family needs to take their first step toward financial clarity.

Michael Rowan is a dedicated writer and researcher specializing in Personal Finance and Investments. With a passion for helping individuals make smarter financial decisions, he creates informative and practical content designed to simplify complex financial topics.